Your #1 Destination

for Online Trading

Next generation broker for traders that aim for excellence!

Access Global Markets with Superior Trading Conditions

40+ years of Group

cumulative experience

Negative balance

protection

Ultra-fast

execution of orders

Professional

Customer Support

Trade the Most Popular Assets

We take great pride in combining some of the best trading conditions in the industry with rapid market execution.

Various order types Super-tight spreads Hedging allowed Maximum fund security Many payment methods

Various order types Super-tight spreads Hedging allowed Maximum fund security Many payment methods CFDs on

Powerful Trading Platforms

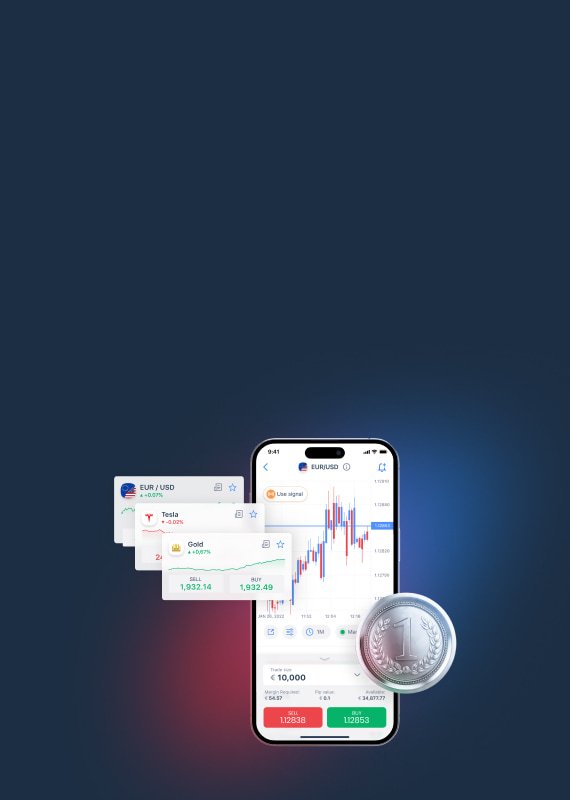

HYCM Trader

Available on Android/iOS.

Our trading app is innovative, clutter-free and intuitive to use. Access and manage all your accounts, discover new opportunities, and trade our range of 300+ instruments directly from your phone. Create personalised price notifications, so you never miss a trade again!

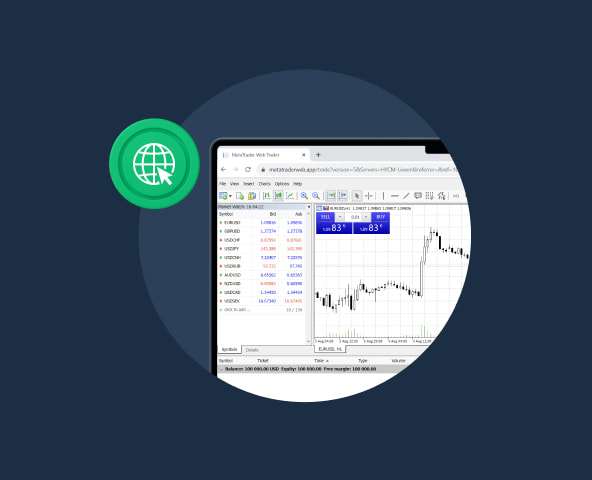

Web Trader

The Web Terminal is available for both MT4 and MT5 users. It allows you to trade from your browser without the need to download any additional software.

MetaTrader 4

Powered by HYCM

Established as the industry standard, it contains everything a trader needs. It offers many features like advanced technical analysis, flexible trading systems, Expert Advisors, as well as a mobile app.

Negative balance protection

Data encrypted by: VeriSign

Client Funds Kept in Tier-1 Banks

25+ Global Awards

Unleash Your Trading Potential with HYCM Trading Account

HYCM Financial Tools

Benefit from our wide range of tools, including calculators and free access to services like Seasonax and Financial Source.

Seasonax

Identify seasonal investment opportunities for 20,000+ stocks, commodities, indices, and currencies with Seasonax.

Financial source

Track market moving events in real time with Financial Source. Stay tuned into what’s moving the markets and uncover the reasons why.

Ready to Get Started

Start trading in 3 easy steps